In his LinkedIn post, the Deputy Minister of Environment and Energy Nikos Tsafos argued against two findings of The Green Tank’s analysis “Trends in Greece’s Retail Electricity Market”, which he described as an “accounting error”. First, he argued that cross-country comparisons of the competitive component of retail electricity prices may be distorted by differences in how costs are allocated between energy and supply charges and network charges across Member States. Second, he questioned the comparison between wholesale and retail electricity prices, suggesting that additional system and network-related costs should be taken into account when interpreting the results.

Following the Deputy Minister’s public comments, The Green Tank would like to present the data and methodology on which its conclusions are based. The response below clarifies the data used and explains why the increased reliance on fossil gas remains a critical issue both for emissions and for the cost of electricity paid by consumers.

First of all, thank you for your kind words. We welcome your constructive criticism of our report “Trends in Greece’s Retail Electricity Market” and the opportunity to contribute to the public debate on an issue of fundamental importance to citizens.

Our responses to the main points raised in your statement are as follows:

- On the alleged “accounting” error

Let us first agree that comparisons among EU Member States always involve important nuances, as each country has its own particular characteristics. For example, you could point out—and we would agree—that Hungary, which appears to have the lowest energy and supply prices according to the same dataset, does not in practice have a competitive retail electricity market and therefore is not directly comparable to other Member States.

Let us also agree that network charges have nothing to do with competition among suppliers in the retail market, as they are regulated charges. The same applies to public service obligation charges, VAT, the Special RES Levy (ETMEAR), environmental taxes, electricity bill subsidies (which many Member States provided to households, particularly during the 2022 energy crisis), or capacity taxes that some Member States (though not Greece) include in electricity bills. These components vary significantly across countries, not only in magnitude but also in the policies adopted.

Consequently, adding all these elements to energy and supply prices and then comparing Member States results in an even greater “accounting” distortion. More importantly, it provides no meaningful insight into how well the retail market is functioning—which is precisely the issue at stake, not only for our analysis but, above all, for providing citizens with accurate information about the only part of their electricity bill they can actually influence: the competitive component, which is determined by the suppliers they choose.

In conclusion, comparing Member States on the basis of energy and supply prices may not be perfect, for the reasons you mentioned, but it remains the best available approach for assessing and comparing the competitive component of retail tariffs across the EU and, by extension, the effectiveness—or lack thereof—of retail market competition.

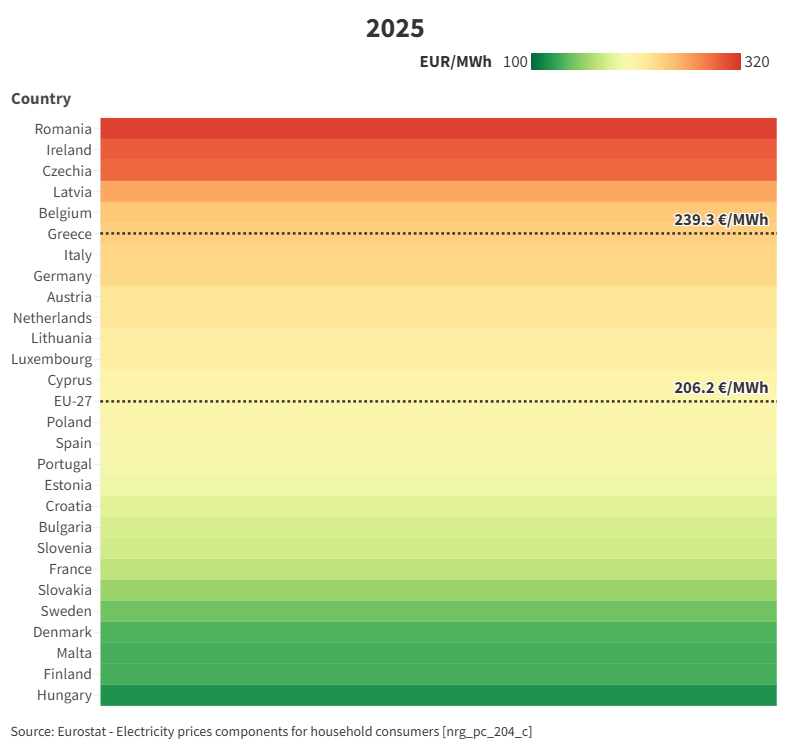

Nevertheless, in order to fully examine your observation, we also compared Member States using the combined value of energy and supply prices plus network charges. We would like to stress that we do not consider this to be a more appropriate comparison, as it mixes the competitive component with regulated charges determined by governments rather than suppliers. However, this aggregation eliminates the “accounting” differences you referred to.

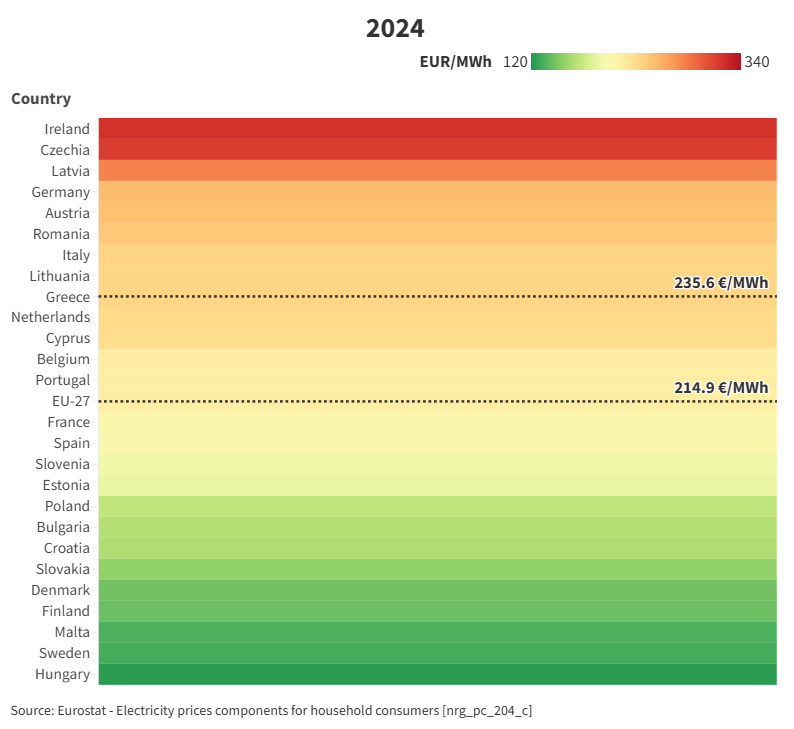

As shown in the chart we provide, Greece ranks as the 6th most expensive country in the EU-27 in 2025 in real terms, that is, when measured according to consumers’ purchasing power, and is 16% more expensive than the EU-27 average. In fact, Greece’s position worsened compared to 2024, when it ranked 9th with €235.6/MWh and was considerably closer to the corresponding EU average (€214.9/MWh).

- On the wholesale–retail comparison

Nowhere do we claim that the difference between wholesale and retail prices represents supplier profits. In fact, all the clarifications that appeared in media coverage of this comparison are explicitly included in our report.

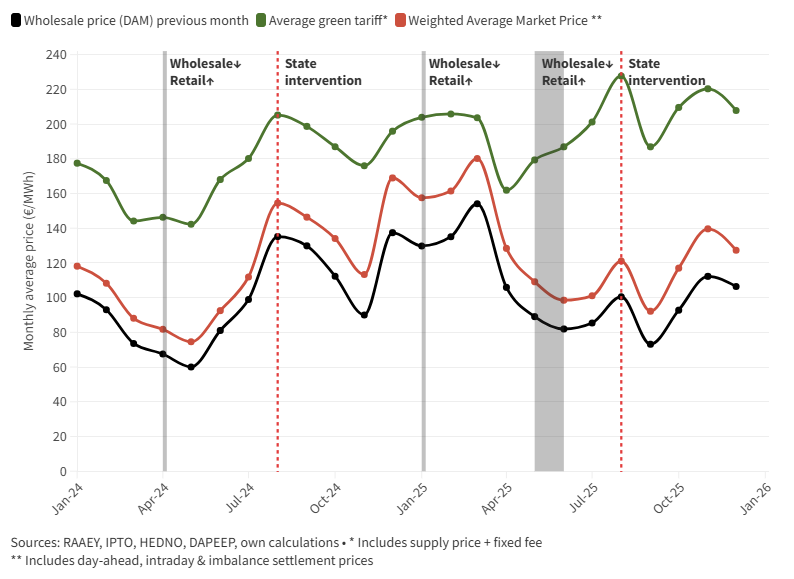

The chart in question illustrates historical trends, and serves as an indicator of changes in suppliers’ profit margins from month to month. The conclusions remain unchanged even if, in addition to the Day-Ahead Market (DAM), one takes into account the intraday market and imbalance settlement charges, as you suggest. To demonstrate this, we provide the same chart using the Weighted Average Market Price, which incorporates all these elements.

As the chart shows:

- Once again, the gap between retail prices (shown in green) and wholesale prices widens significantly from spring 2025 onwards, displaying exactly the same peaks and troughs.

- Once again, during the same months in which wholesale prices were declining, retail prices were increasing.

- Once again, we observe the same weak market response to the two most significant government interventions.

- Beyond these points

We hope you will agree with us on the broader picture: the retail electricity market in Greece is not functioning satisfactorily.

For example, it is not a sign of a healthy market that around 80–90 retail electricity products are available each month, yet only 6–7 of them offer time-of-use (bizonal) pricing—and 2–3 of those provide only minimal price differentiation between time zones. This is occurring more than a year after the introduction of the new “night tariff” time periods, which include a mid-day low price zone. How can consumers be incentivized to shift their consumption to midday hours, and how can renewable energy curtailments be reduced under such conditions?

Nor is it a sign of a healthy market that six out of ten households remain on the more expensive green tariffs, while Greece ranks among the worst-performing countries in the EU-27 in terms of households’ inability to pay utility bills, according to Eurostat. Citizens need more information—and more responsible information.

We hope that addressing these serious shortcomings, which ultimately impose additional costs on households and businesses, will become a key priority of your policy agenda in the coming period.

We remain at your disposal and stand ready to contribute in any way we can toward this objective.